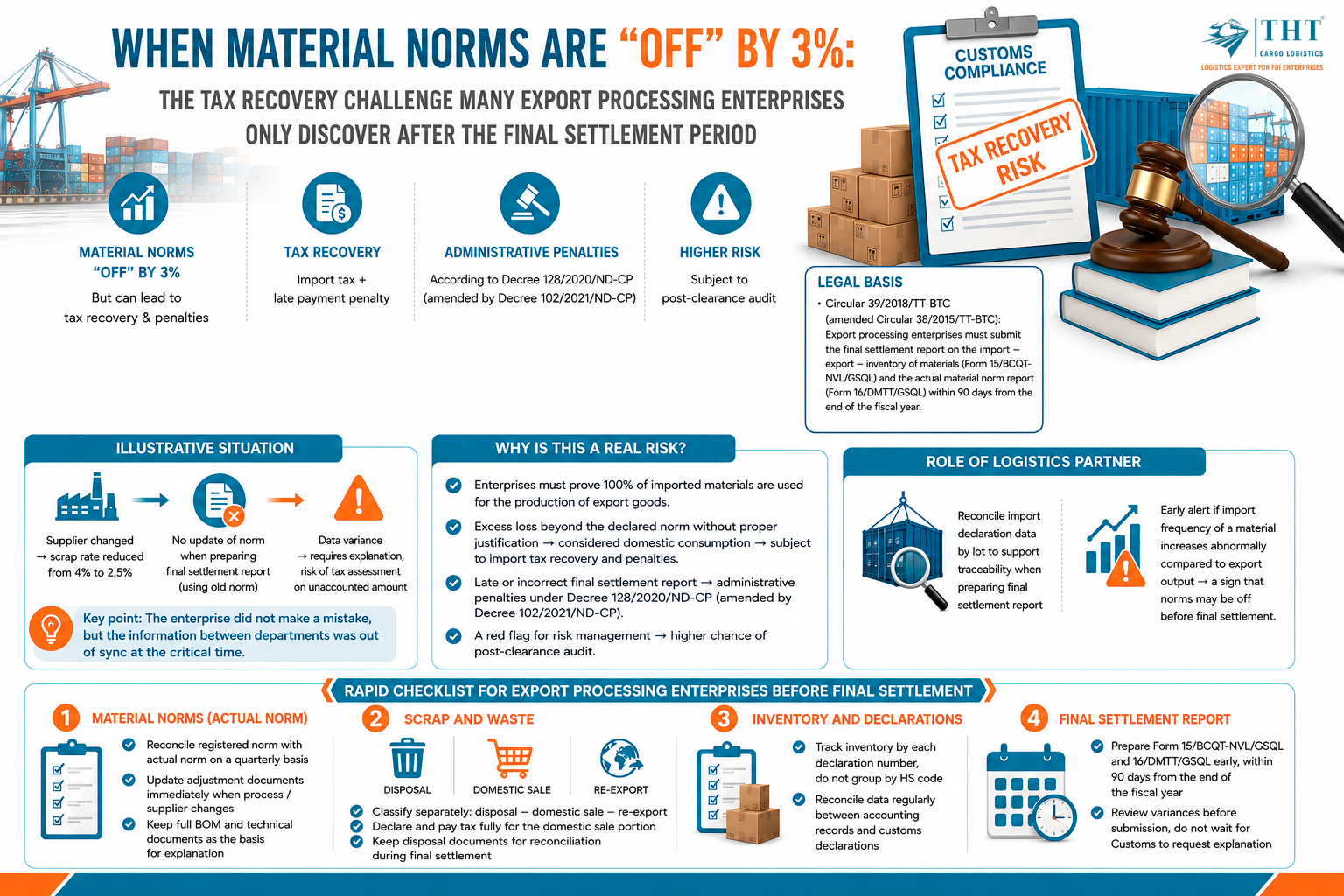

- When a 3% Material Consumption Variance Leads to Customs Tax Reassessment: A Risk Many Export Processing Enterprises Discover Only During Year-End Finalization

- Why Is This a Real Compliance Risk?

- Illustrative Case Study

- Three Areas Export Processing Enterprises Should Review Immediately

- Three Areas Every Export Processing Enterprise Should Review Before Year-End

- How an Experienced Logistics Partner Can Help Reduce Compliance Risks

- Quick Compliance Checklist Before Annual Customs Settlement

- Conclusion

- Need Support with Customs Compliance for Your Export Processing Enterprise?

When a 3% Material Consumption Variance Leads to Customs Tax Reassessment: A Risk Many Export Processing Enterprises Discover Only During Year-End Finalization

THT Cargo Logistics — Customs Compliance Insights for FDI Enterprises

This is a situation THT Cargo Logistics has encountered repeatedly while supporting Export Processing Enterprises (EPEs) across Southern Vietnam’s industrial parks. The production department improves manufacturing processes, changes raw material suppliers, or adjusts production formulas to reduce scrap rates—positive operational improvements in every sense. However, if the import-export department does not update the registered material consumption norms with Customs, a hidden gap gradually forms between the declared consumption rate and the actual production consumption.

This discrepancy usually goes unnoticed throughout the year. It only becomes apparent when the enterprise prepares its Annual Customs Finalization Report or, even worse, when Customs officers request a reconciliation during a post-clearance audit.

Key Takeaway:

Even minor improvements in production efficiency can create compliance risks if the registered Bill of Materials (BOM) or material consumption norms are not updated in time. What appears to be a small operational change today may result in tax reassessment months later.

Why Is This a Real Compliance Risk?

Under Vietnam’s customs regulations governing duty exemption for imported raw materials used in export production, the burden of proof lies with the enterprise. Companies must demonstrate that all duty-exempt imported materials have been used exclusively for manufacturing exported products.

This requirement is stipulated in Circular No. 39/2018/TT-BTC (amending Circular No. 38/2015/TT-BTC), which requires Export Processing Enterprises to submit:

- The Annual Import–Export–Inventory Finalization Report for raw materials (Form 15/BCQT-NVL/GSQL).

- The Actual Material Consumption Norm Report for exported products (Form 16/ĐMTT/GSQL).

Both reports must be submitted within 90 days after the end of the company’s fiscal year.

If the difference between imported materials and actual production consumption exceeds the registered consumption norms and the enterprise cannot provide sufficient technical justification, Customs authorities may treat the unexplained quantity as domestic consumption. This may result in import duty reassessment together with late payment interest.

In addition, late submission or inaccurate declaration of the Customs Finalization Report may lead to administrative penalties under Decree No. 128/2020/NĐ-CP (as amended by Decree No. 102/2021/NĐ-CP). It may also increase the company’s customs risk profile, making it more likely to be selected for future post-clearance audits.

Enterprises Should Pay Particular Attention To:

- Ensuring registered material consumption norms accurately reflect actual production.

- Updating Customs records whenever production processes or material suppliers change.

- Maintaining complete technical documentation to support explanations during Customs inspections.

Illustrative Case Study

(Based on common industry scenarios and not referring to any specific enterprise.)

An electronics Export Processing Enterprise located in Southern Vietnam changed its plastic component supplier, successfully reducing its production scrap rate from 4% to 2.5%. Operationally, this was an excellent manufacturing improvement.

However, the import-export department continued using the old material consumption norms in the Customs Finalization Report because the production team had not communicated the change internally.

When preparing the year-end Customs Finalization Report, discrepancies appeared between the accounting inventory records and the figures reported to Customs.

Since the company could not provide updated engineering documents (such as the revised Bill of Materials) showing when the production norm had changed, it was required to submit additional explanations. This significantly prolonged the review process and exposed the company to the risk of Customs imposing additional import duties on any unexplained material differences.

Key Lesson:

The issue was not that the company intentionally violated Customs regulations. The real problem was the lack of timely communication and coordination between internal departments when operational changes occurred.

Three Areas Export Processing Enterprises Should Review Immediately

1. Compare Registered Consumption Norms with Actual Production Regularly

Enterprises should compare their registered material consumption norms with actual production data on a regular basis—preferably every quarter rather than waiting until year-end finalization.

Whenever production processes, manufacturing formulas, or material suppliers change, the registered consumption norms should be updated before subsequent import or production activities take place. Retroactive adjustments after Customs inspections have begun are rarely accepted.

2. Clearly Classify Scrap and Waste Materials

Manufacturing scrap and waste should be clearly categorized into three separate groups:

- Destruction.

- Domestic sale (subject to Customs declaration and applicable taxes).

- Re-export.

Combining these categories into a single accounting item is a common compliance issue that often leads to additional clarification requests during Customs reviews.

3. Track Inventory by Individual Customs Declaration

Raw material inventory should be monitored based on individual Customs declaration numbers rather than being aggregated solely by material codes.

During post-clearance audits, Customs authorities frequently require enterprises to trace imported materials back to specific Customs declarations in order to reconcile commercial invoices, bills of lading, payment records, and related import documentation.

Three Areas Every Export Processing Enterprise Should Review Before Year-End

1. Compare Registered Consumption Norms with Actual Production Regularly

Instead of waiting until year-end settlement, companies should compare their registered material consumption norms with actual production data on a regular basis (quarterly reviews are recommended).

Whenever there are changes in production processes, formulas, or raw material suppliers, the production norm should be updated before subsequent import shipments are processed. Attempting to adjust norms retroactively after a customs inspection has begun is rarely accepted.

2. Classify Scrap and Waste Materials Properly

Scrap and waste materials should be clearly classified into three categories:

- Materials destroyed.

- Materials sold into the domestic market (subject to customs declaration and applicable taxes).

- Materials re-exported.

Combining these different categories into a single accounting item is one of the most common reasons customs authorities request additional explanations during customs settlement reviews.

3. Track Inventory by Individual Import Declaration

Inventory should be monitored based on each customs declaration number rather than being consolidated solely by material code.

During post-clearance audits, customs authorities frequently require enterprises to trace imported materials back to individual customs declarations in order to reconcile invoices, bills of lading, payment records, and inventory movement.

Key Recommendation

Regular internal reconciliation between production, import-export, accounting, and warehouse departments can identify discrepancies early, allowing corrective actions before annual customs settlement or post-clearance inspections.

How an Experienced Logistics Partner Can Help Reduce Compliance Risks

Beyond transportation services, an experienced logistics provider specializing in Export Processing Enterprises (EPEs) can contribute significantly to customs compliance.

By maintaining detailed import declaration records for each shipment, logistics partners can help enterprises retrieve historical customs data more efficiently when preparing annual customs settlement reports.

In addition, continuous monitoring of import trends may reveal abnormal increases in imported raw materials compared with export production volumes—an early warning sign that registered production norms may no longer reflect actual manufacturing conditions.

Identifying these inconsistencies early allows enterprises to review and update production norms before customs authorities discover the discrepancy during inspections.

Quick Compliance Checklist Before Annual Customs Settlement

Material Consumption Norms

- ☐ Compare registered production norms with actual production data every quarter.

- ☐ Update adjustment documents immediately whenever production processes or suppliers change.

- ☐ Maintain complete Bills of Materials (BOMs) and technical documentation to support future customs explanations.

Scrap and Waste Materials

- ☐ Separate materials into destruction, domestic sale, and re-export categories.

- ☐ Declare and pay applicable taxes for materials sold domestically.

- ☐ Retain all supporting documents related to scrap handling and disposal.

Inventory and Customs Declarations

- ☐ Track inventory by individual customs declaration rather than only by material code.

- ☐ Regularly reconcile accounting records with customs declaration data.

Annual Customs Settlement Report

- ☐ Prepare Forms 15/BCQT-NVL/GSQL and 16/ĐMTT/GSQL well in advance.

- ☐ Submit reports within 90 days after the end of the fiscal year.

- ☐ Review and resolve discrepancies before submission instead of waiting for customs requests.

Conclusion

A deviation of only a few percentage points in material consumption may appear insignificant from a production perspective, but from a customs compliance perspective, it can become a tax exposure that is only discovered during annual customs settlement or post-clearance audit.

For Export Processing Enterprises, customs compliance is not solely the responsibility of the import-export department. It requires close coordination among production, planning, accounting, warehouse, procurement, and logistics teams to ensure that actual manufacturing activities remain consistent with customs declarations.

Early monitoring, timely updates, and systematic record management remain the most effective approaches to minimizing customs risks while maintaining uninterrupted manufacturing operations.

Need Support with Customs Compliance for Your Export Processing Enterprise?

THT Cargo Logistics works closely with FDI manufacturers to support customs compliance, annual customs settlement preparation, import declaration reconciliation, customs documentation review, and risk assessment throughout import-export operations.

Our experienced customs specialists help enterprises strengthen compliance, reduce post-clearance audit risks, and maintain stable production without unexpected customs issues.

Visits: 8