- OFFICIAL LETTER No. 17769/CHQ-NVTHQ: GUIDELINES ON CUSTOMS PROCEDURES AND TAX POLICIES FOR EXPORT PROCESSING ENTERPRISES (EPEs)

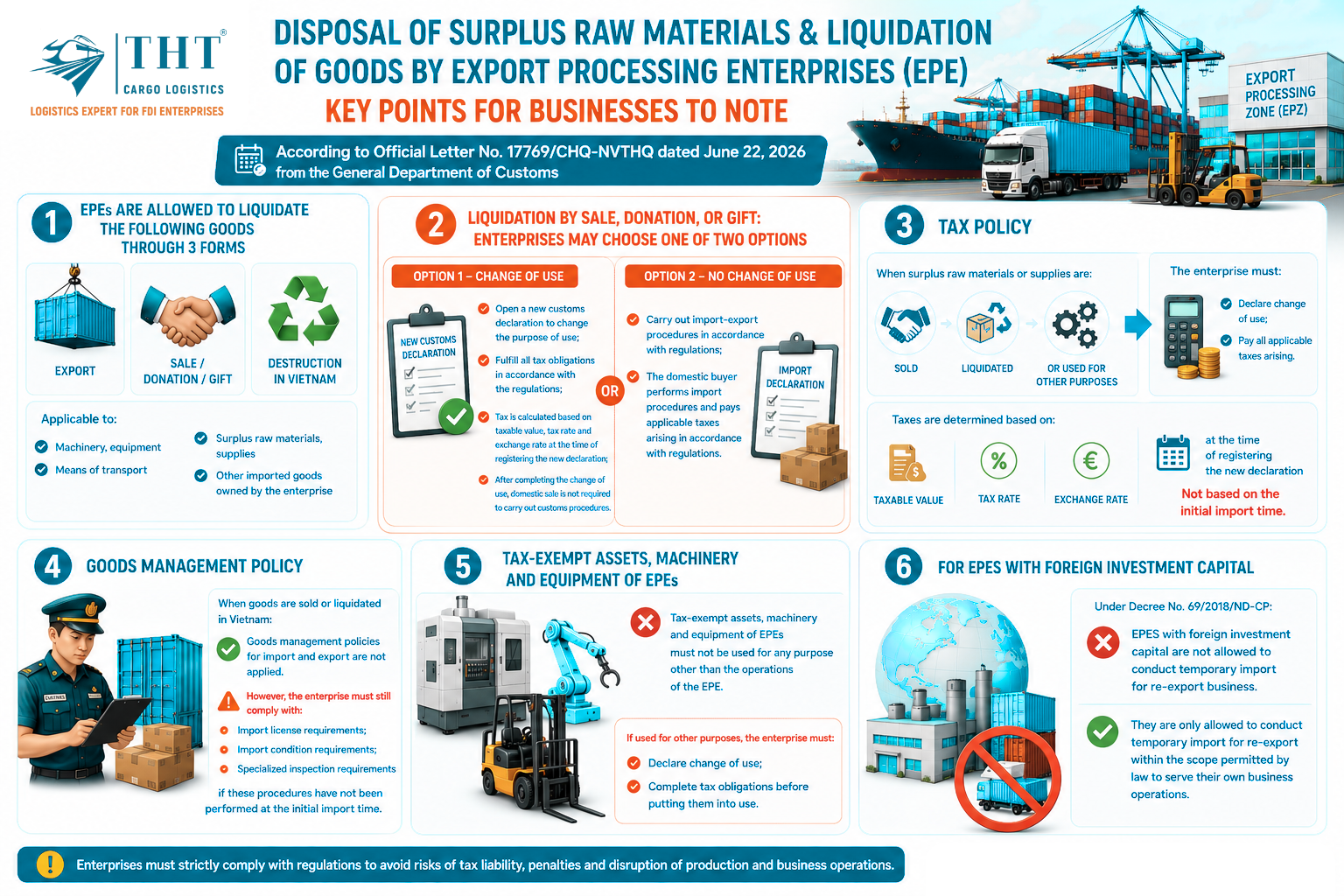

- 1. What Types of Goods Can an Export Processing Enterprise (EPE) Liquidate?

- 2. Customs Procedures for Each Liquidation Method

- 3. Tax Policy for Surplus Raw Materials and Supplies

- 4. Goods Management Policy for Domestic Sale or Liquidation

- 5. Regulations on Duty-Exempt Assets, Machinery, and Equipment of Export Processing Enterprises

- 6. Regulations for Foreign-Invested Export Processing Enterprises

- Key Takeaways for Export Processing Enterprises

- Need Advice on EPE Goods Liquidation or Change of Intended Use?

OFFICIAL LETTER No. 17769/CHQ-NVTHQ: GUIDELINES ON CUSTOMS PROCEDURES AND TAX POLICIES FOR EXPORT PROCESSING ENTERPRISES (EPEs)

On June 22, 2026, the Customs Department issued Official Letter No. 17769/CHQ-NVTHQ, providing guidance on customs procedures, tax policies, and the handling of surplus raw materials, supplies, machinery, equipment, and assets owned by Export Processing Enterprises (EPEs).

This official guidance is of particular interest to FDI enterprises, Export Processing Enterprises (EPEs), and export manufacturing businesses, as it clarifies numerous issues relating to goods liquidation, changes in the intended use of imported goods, tax obligations, and customs management policies.

📄 Download Official Letter No. 17769/CHQ-NVTHQ

Businesses may download the full Official Letter for detailed guidance issued by the Customs Department.

1. What Types of Goods Can an Export Processing Enterprise (EPE) Liquidate?

According to Official Letter No. 17769/CHQ-NVTHQ, Export Processing Enterprises are permitted to liquidate various types of assets and goods owned by the enterprise.

These include:

- Machinery and equipment.

- Means of transport.

- Raw materials.

- Supplies.

- Other imported goods owned by the enterprise.

An enterprise may choose one of the following liquidation methods:

- Export.

- Sale.

- Donation or gifting.

- Destruction within Vietnam.

2. Customs Procedures for Each Liquidation Method

a. Liquidation by Export

Businesses shall complete export customs procedures in accordance with current regulations for goods leaving the territory of Vietnam.

b. Liquidation by Sale, Donation, or Gift

For goods that are sold, donated, or gifted, enterprises may choose one of the following two options:

Option 1 – Change the Intended Use

- Register a new customs declaration to change the intended use of the goods.

- Fulfill all applicable tax obligations in accordance with regulations.

- Taxes shall be determined based on the customs value, applicable tax rate, and exchange rate at the time the new customs declaration is registered.

- After the change of intended use has been completed, the subsequent domestic sale of the goods is not subject to additional customs procedures.

Option 2 – Without Changing the Intended Use

- Complete the required export and import customs procedures in accordance with regulations.

- The domestic purchaser is responsible for carrying out the import customs procedures.

- The domestic purchaser must fulfill all applicable tax obligations as prescribed by law.

c. Liquidation by Destruction

Goods must be destroyed in accordance with current regulations and under the supervision of the customs authority throughout the entire destruction process.

3. Tax Policy for Surplus Raw Materials and Supplies

One of the key topics clarified in Official Letter No. 17769/CHQ-NVTHQ is the tax policy applicable to surplus raw materials, supplies, or goods that are converted to purposes other than their original export manufacturing purpose.

According to the General Department of Customs’ guidance, if surplus raw materials or supplies are sold, liquidated, or used for other purposes, the enterprise must fulfill all applicable tax obligations in accordance with current regulations.

Required Actions for Enterprises

- Declare the change in the intended use of the goods.

- Pay all applicable taxes as required by law.

- Taxes shall be determined based on the customs value, applicable tax rate, and exchange rate at the time the new customs declaration is registered.

- The customs value, tax rate, and exchange rate applicable at the original importation date shall not be used.

This clarification is particularly important for Export Processing Enterprises (EPEs), as many businesses mistakenly believe that taxes should be calculated based on the original import declaration. However, Official Letter No. 17769/CHQ-NVTHQ clearly states that the tax liability is determined at the time the enterprise registers the declaration for the change of intended use.

4. Goods Management Policy for Domestic Sale or Liquidation

In addition to tax regulations, the Official Letter also clarifies the management policies applicable when Export Processing Enterprises sell or liquidate goods within the Vietnamese market.

Accordingly:

- Import and export goods management policies do not apply to domestic sales or liquidation activities.

- However, enterprises must still comply with import licensing requirements, import conditions, or specialized inspections if these procedures were not completed at the time of the original importation.

Important Note:

The exemption from import and export goods management policies does not mean that enterprises are exempt from sector-specific regulatory requirements. If the goods are subject to specialized management, all applicable regulations must still be fully satisfied before the goods can be sold in the domestic market.

5. Regulations on Duty-Exempt Assets, Machinery, and Equipment of Export Processing Enterprises

For assets, machinery, and equipment that enjoy duty exemption under the Export Processing Enterprise regime, the Official Letter continues to emphasize the requirement that these assets must be used for their intended purposes.

Specifically:

- Duty-exempt assets, machinery, and equipment may only be used to support the operations of the Export Processing Enterprise itself.

- They must not be used for any purpose outside the enterprise’s approved business activities.

If the enterprise intends to use these assets for another purpose, it must:

- Declare the change of intended use with Customs.

- Complete all applicable tax obligations before putting the assets into use.

These requirements are intended to ensure the proper application of investment incentive policies for Export Processing Enterprises while preventing the misuse of duty-free assets outside the permitted scope.

6. Regulations for Foreign-Invested Export Processing Enterprises

For foreign-invested Export Processing Enterprises, Official Letter No. 17769/CHQ-NVTHQ also refers to the provisions of Decree No. 69/2018/ND-CP governing temporary import for re-export activities.

Accordingly:

- Foreign-invested Export Processing Enterprises are not permitted to conduct temporary import for re-export trading activities.

- They may only carry out temporary import for re-export activities where permitted by law and solely to support their own production and business operations.

Enterprises should clearly distinguish between activities serving their own manufacturing operations and commercial trading activities in order to avoid customs compliance risks or violations of investment regulations.

Key Takeaways for Export Processing Enterprises

Official Letter No. 17769/CHQ-NVTHQ demonstrates Customs’ continued focus on strengthening the management of duty-exempt goods, surplus raw materials, machinery, equipment, and liquidation activities carried out by Export Processing Enterprises.

To minimize operational and compliance risks, enterprises are encouraged to:

- Review internal procedures for managing duty-free assets and imported raw materials.

- Select the appropriate liquidation method before initiating any transaction.

- Assess potential tax obligations before changing the intended use of goods.

- Prepare complete documentation for sales, liquidation, or destruction activities.

- Verify whether specialized import requirements apply before selling goods into the domestic market.

- Work closely with experienced logistics providers and customs consultants to determine the most appropriate compliance approach from the outset.

Need Advice on EPE Goods Liquidation or Change of Intended Use?

THT Cargo Logistics assists Export Processing Enterprises in reviewing customs regulations, evaluating liquidation options, advising on changes of intended use, determining tax obligations, and preparing complete customs documentation to ensure full compliance while minimizing operational risks.

With extensive experience supporting FDI manufacturers and Export Processing Enterprises in customs compliance, bonded warehouse management, annual settlement reporting, and cross-border logistics, THT helps businesses implement the most suitable solution, optimize costs, and comply with Vietnam Customs regulations.

Visits: 36